Samsung Electronics: Smartphone Recovery Pace In Q3 The Decisive Factor

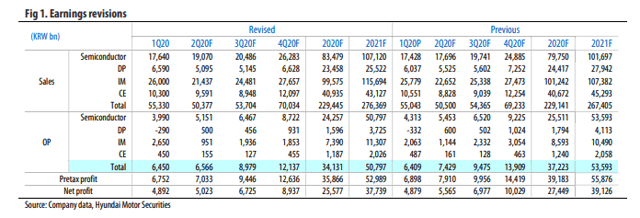

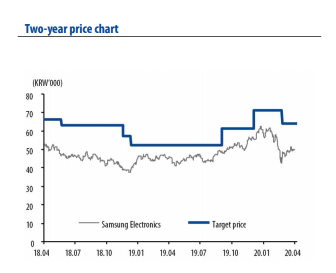

We maintain BUY and our six-month-forward target price of KRW64,000 (1.6x 2020F BPS attributable to controlling interest) on Samsung Electronics (OTC:SSNLF). Samsung reported KRW55.3tn in sales and KRW6.45tn in operating profit for 1Q20. By division, IM's operating profit of KRW2.65tn was 29% higher than our estimate helped by the sell-in effect from the Galaxy S20 Ultra, while semiconductor's operating profit stood at KRW4tn. We are particularly encouraged by the robust sales growth (+50% YoY to KRW4.5tn) of system LSI and foundry (including LED).

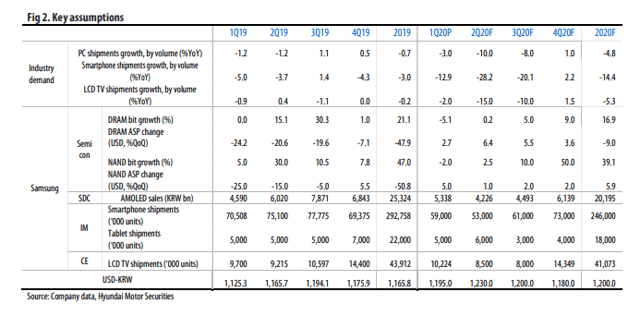

In system LSI, 108-megapixel image sensors helped fuel CIS sales growth, and 5G modem and PMIC also enjoyed modest sales. CIS and 5G modem sales should continue to grow given the expected growth of demand for mid/low-end 5G smartphones in 2H20. We now estimate CIS sales for 2020 will jump more than 30% YoY to around KRW4tn on the growing sales of multiple cameras and high-pixel cameras. For 2Q20, sales will likely retreat 9% QoQ to KRW50.3tn on dwindling smartphone demand as offline stores close amid lockdowns across the globe. As for operating profit, the IM division will probably see a decline in operating profit but we expect overall operating profit to keep up QoQ at KRW6.6tn thanks to a provision writeback in the OLED division. However, uncertainty remains considering the low visibility of smartphone demand.

In system LSI, 108-megapixel image sensors helped fuel CIS sales growth, and 5G modem and PMIC also enjoyed modest sales. CIS and 5G modem sales should continue to grow given the expected growth of demand for mid/low-end 5G smartphones in 2H20. We now estimate CIS sales for 2020 will jump more than 30% YoY to around KRW4tn on the growing sales of multiple cameras and high-pixel cameras. For 2Q20, sales will likely retreat 9% QoQ to KRW50.3tn on dwindling smartphone demand as offline stores close amid lockdowns across the globe. As for operating profit, the IM division will probably see a decline in operating profit but we expect overall operating profit to keep up QoQ at KRW6.6tn thanks to a provision writeback in the OLED division. However, uncertainty remains considering the low visibility of smartphone demand.

Major issues and earnings outlook

Major issues and earnings outlook

A key point to note going forward is the rapidity of smartphone demand recovery when social distancing campaigns across the world ease in 3Q20. Samsung's components, including memory chips, system semiconductors (CIS, AP, foundry), and mobile OLED are heavily dependent on smartphone demand. While solid demand for servers and PCs provide firm downside support for earnings, the key swing factor for Samsung's earnings, in our view, will be smartphone demand. We note that there will be intense competition among Samsung, Apple, and Huawei in 2H20, which will determine each company's earnings for 2020. Consequently, marketing costs will rise and profitability will not improve as fast as desired. Having said that, a recovery of smartphone demand will provide decisive momentum for the company's semiconductor and mobile OLED businesses.

Share price outlook and valuation

Share price outlook and valuation

In the long term, the semiconductor division's growth momentum will be highlighted even further going forward as it stands to benefit massively from the "untact" movement. In the near term, we advise investors to buy and hold the stock on the potential for earnings improvement in 2H20 with smartphone demand hitting the bottom in 2Q20.

Komentar

Posting Komentar